Mily Vázquez Harkivi

This article is CC licensed Attribution-NonCommercial-ShareAlike 4.0 International.

A voluntary practice in the 20th century, sustainability reporting became standardized and mandatory in the 21st century. Nevertheless, mandatory reporting does not guarantee corporate responsibility. Deficient sustainability reporting can mislead stakeholders and result in inaccurate performance assessments (Herremans, 2020). Research conducted on the Corporate Sustainability Reporting Directive introduced recently by the European Union shows a lack of transparency in sustainability reports (Correa-Mejía et al., 2024). Research shows deficiencies in the disclosure of the Double Materiality Assessment process, which is the key to the new directive (Mio et al., 2024).

The purpose of this article is to explore challenges and opportunities encountered when conducting a Double Materiality Assessment. The paper explores this process with data gathered by interviewing a total of six individuals working in fields directly related to sustainability. Three experts and three sustainability professionals were contacted and interviewed from February to November 2024. Findings reveal that understanding of the Double Materiality Assessment process varies, highlighting both the ambiguity of the process and its adaptability to different contexts. Challenges of the DMA process include resource limitations, data structuring, and recognizing impacts occurring in the value chain. The article is part of the author’s article thesis for the MBA in Management in Sustainable Business at Häme University of Applied Sciences (HAMK).

1 Introduction

Sustainability and sustainable development are concepts connected to the economic and political systems. Schoenmaker & Schramade (2019, p. 17) argue that sustainability cannot be understood in isolation from the socioecological system in which it is embedded. Recognizing the importance of sustainability, the European Union has been a leader in regulating sustainability reporting. A significant change came in 2014 with the introduction of the Non-Financial Reporting Directive (Fälth & Lindberg, 2024). The EU Green Deal was introduced to support economic activity aligned with the environmental goals of the region (EU Green Deal, n.d.).

The European Commission (EC) continued the regulation of sustainability reporting, which led to the introduction of the Corporate Sustainability Reporting Directive (CSRD). This directive represents a pivotal shift in sustainability reporting, affecting companies from EU member states and foreign companies operating within the EU region. The European Sustainability Reporting Standards (ESRS) introduced by the directive cover a wide range of data considered ‘material’ (relevant) for organizations from a sustainability perspective.

A change of paradigm was the introduction of the double materiality perspective where companies assess their operations to identify topics that are material from both an impact (inside-out) and financial (outside-in) perspective. This perspective entails the Double Materiality Assessment (DMA) process, referring to the analysis of a company’s operations and sustainability.

This article aims to make the DMA process valuable for companies moving beyond mere compliance. By outlining the challenges and opportunities of the DMA process, companies can review their operations and strategy and align them to support their sustainability goals.

1.1 Background

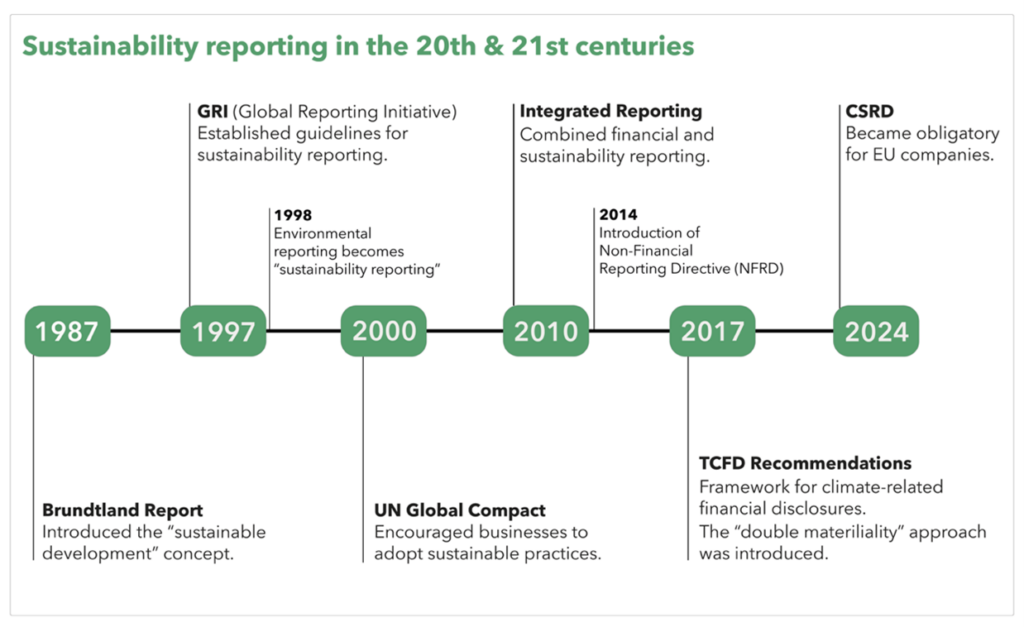

Companies have been reporting about their sustainability for decades. Figure 1 shows key points of sustainability reporting during the 20th and 21st century. Early sustainability reports show deficits in methodological rigour, external assurance, and uniformity across industries.

The concept of materiality originates from the field of accounting, and it is also considered a legal term (Uwah, 2024, p. 34). Puroila and Mäkelä (2019) highlight the purpose of materiality and argue that focusing on issues that matter increases transparency and accountability. One key question is how companies identify sustainability issues and what methodologies they utilize to identify them. Jørgensen et al. (2022) contend that companies identify issues by applying varied methodologies. Correa-Mejíaet al. (2024) state that materiality depends on how each company performs the assessment and under what guiding standards. The identification of material issues is crucial, as well as the methodologies employed to identify them.

Correa-Mejíaet al. (2024) stressed the two sides of materiality: the financial perspective that identifies what may affect the financial performance and impact materiality in which companies assess their impacts on the environment. The EC introduced the term ‘double materiality’ to link both (Correa-Mejíaet al., 2024, p. 5). Sustainability reporting is inherently complex (De Villiers, 2022), and the concept of double materiality adds further complexity. Nevertheless, Puroila and Mäkelä (2019) argue that materiality plays a crucial role in the organization’s sustainability strategy.

The DMA process starts by getting familiar with the ESRS 1 and the section outlining the DMA. The standard outlines the matters to include and to measure. The ESRS 1 states that the DMA contemplates the impacts of the company and the impacts to the company in the short, medium and long term. Research analysing the DMA sections of sustainability reports identified inconsistencies related to early adopters of the DMA process (Correa-Mejía, 2024). Mio et al. (2024) encountered vague explanations of the DMA process in the reports.

The theories utilized to analyse sustainability reporting are legitimacy theory (Suchman, 1995), stakeholder theory (Freeman, 2010; Eskerod, 2020), institutional (Roszkowska-Menkes, 2022), and signalling theory (Friske et al., 2022). Nevertheless, following the argument of Fiandrino et al. (2022) theoretical background related to materiality is diverse. Surprisingly, research shows that almost half of the studies related to materiality are not based on a theoretical background.

A predominant theory utilized in the research related to materiality is that of stakeholder theory, followed by legitimacy theory (Fiandrino et al., 2022). Stakeholder theory is particularly relevant for the study of CSRD because the purpose of moving sustainability reporting from a voluntary endeavour to a legal obligation also responds to stakeholder’s demands.

Legitimacy theory highlights important dimensions like the organization’s cultural norms, symbols, beliefs, and rituals. Legitimacy affects not only how people act towards organizations but also how they understand them. (Suchman, 1995, p. 571). Institutional theory analyses organizational behaviour and explains how rules, structures, and processes affect the organization more than the market. Institutional theory is connected to legitimacy theory since it assumes that through following rules and processes organizations are seeking legitimacy (Roszkowska-Menkes, 2022).

Signalling theory studies the information asymmetries between signallers (i.e., managers) and receivers (i.e., interested stakeholders). A sustainability report can be considered a signal that can evoke trust or damage it, for example, ‘greenwashing’ is considered a false signal. (Friske et al., 2022).

1.2 Research questions

This article argues that various challenges related to the DMA process can emerge in several companies. The research questions are those mentioned in the author’s MBA article-thesis:

- How do companies reporting the financial year 2024 (i.e. publishing report in 2025) in Finland conduct a double materiality assessment?

- Which approach they take to the challenges identified when conducting a double materiality assessment?

- Are opportunities linked to the business strategy being identified?

The article is divided into four sections followed by conclusions. The first section introduced the reader to the theoretical background underpinning sustainability reporting and illustrated key concepts. The second section will explain the methodology followed and the data collection process. The third section shows the results of the data analysis. The fourth section discusses and suggests insights about the process, challenges, and opportunities of the DMA.

2 Methodology and data collection

This qualitative research is interpretive; it considers ‘alternative viewpoints and factors unique to the context’ (Lee & Lings, 2008, p. 66), for instance, the fact that the subject of concern (CSRD and DMA) is novel and in development within the business context. The interpretive position ‘considers its findings to represent one of many possible representations’ (Lee & Lings, 2008, p. 66). Nevertheless, the author was strict not to let its own biases, interests, or prejudices affect the interpretation of the data. A grounded theory strategy was applied to capture the complexity and generate theory from the data (Bell et al., 2022, p. 539).

The data collection started by contacting a total of six individuals who work in areas directly related to sustainability. All interviewees were contacted directly by email, for example, through common contacts. One interviewee was contacted through MS Teams messaging after being invited to participate at the end of a webinar focused on the CSRD. All interviewees were based in Finland except one sustainability professional based in Sweden. Three of the interviewees were classified as experts due to their broad knowledge and expertise in sustainability-related themes. The other three interviewees were classified as sustainability professionals due to their work in fields related to sustainability and sustainability reporting; they were highly knowledgeable in environmental topics, sustainable finance, and quality management and applied this knowledge in sustainability reporting. Nevertheless, all interviewees, experts and professionals, are familiar with areas related to sustainability, sustainability reporting, and the newly introduced Corporate Sustainability Reporting Directive.

The interviews lasted approximately 45 minutes and were conducted through MS Teams. Following the arguments by Lee & Lings (2008, p. 236) the first steps in analysis occurred before data collection started with a theoretical understanding of the questions to ask and how to ask them. An initial literature review provided ideas about what matters could be explored during the interviews and could answer the research questions. An interview guide was designed before the data collection started; it outlines the topical areas and list of issues to address during the interviews (Bell et al., 2022, p. 590). The questions started with and introduction that covered the professional background and the knowledge of sustainability reporting of the interviewees. Then the interview guide was divided into three sections: knowledge about CSRD, knowledge about the application of CSRD (including the double materiality assessment), and knowledge about the consequences of CSRD in local (national) legislation.

The last interviews were highly iterative. According to Bell et al. (2022, p. 588) constant comparison as a tool for grounded theory involves comparing new and existing data, concepts and categories. The ideas that have already emerged from the analysis of the previous interviews had a relevant role to play (Bell et al., 2022, p. 590). Concepts like ‘challenges’ and ‘change’ when conducting a DMA had already emerged in the first interviews and these provided a hint of what topics could be explored in the subsequent interviews.

When analysing the data, initial codes were extracted: each transcript was analysed and rich insights related to the research questions were highlighted. After analysing the six interviews it was evident that varied but consistent ideas, concepts, and themes related to the DMA process and challenges were surfacing. A total of six thematic codes were identified throughout the interviews. The first thematic code relates to the changes in sustainability reporting originating from the introduction of CSRD. Subtopics related to this theme included mentions of local legislation, language of the report, early DMA adoption, reporting on a ‘compliance level’, challenges for SMEs, and the use of consultants.

The second code identified is related to the professional background of the participant. It includes subtopics like know-how, lack of formal expertise in reporting and/or recent experience, and ‘on-the-job’ learning. The third code is DMA as a basis for CSRD and the theme focused exclusively on stakeholder engagement. The fourth code was the DMA process; it included subtopics related to the tools, processes, and methodologies utilized in the DMA process. The fifth code identified the challenges in the DMA process; the subtopics relate to resources that emphasise time. The last thematic code is the development after the process, and it includes the identification of areas of improvement.

After these initial pattern codes were identified, concepts and themes related to the DMA process and challenges were extracted. In the next section, some of the interviewee’s excerpts are mentioned, and the themes are analysed.

3 Results

The findings are presented in two subsections. The first shows the findings related to the DMA process and the second addresses the challenges and opportunities.

3.1 Dimensions of the DMA process

A total of nine themes related to the DMA process were identified after analysing the data. The themes and frequency of concepts identified in the data are presented in Table 1. The themes are listed in the table and all the concepts from which the themes arise are listed in Attachment 1 (experts) and Attachment 2 (sustainability professionals). The attachments show the concepts extracted from the data analysis; for example, phrases like ‘Should be easy to verify claims company make’ and ‘Many discussions about resourcing’ were classified into the ‘Focus on effectiveness’ theme. Most of the concepts recur throughout the data, except for the one classified as ‘Focus on hermeneutics,’ which was mentioned only in one interview.

Salient themes are ‘Focus on effectiveness’, ‘Focus on anticipation’, and ‘Focus on compliance’. This could imply that both experts and professionals emphasize the results, anticipate the needs to get the results, and have in mind that the process responds to the need to comply with the CSRD.

Table 1. DMA process – Themes and total frequency of concepts.

| Themes | Experts | Sustainability professionals |

|---|---|---|

| Focus on accuracy and assurance | 2 | 1 |

| Focus on anticipation | 3 | 2 |

| Focus on compliance | 2 | 2 |

| Focus on effectiveness | 11 | 8 |

| Focus on hermeneutics | 2 | 0 |

| Focus on internal cooperation | 2 | 2 |

| Focus on the strategy of the organization | 4 | 1 |

| Focus on sustainability performance | 1 | 3 |

| Focus on external cooperation | 0 | 2 |

The findings suggest that there are differences in the focus areas of experts and sustainability professionals. The experts focus more on the strategy of the organization than the sustainability professionals. Sustainability professionals focus more on sustainability performance and external cooperation. The experts focus more on accuracy and assurance as well as ‘anticipation’ than the sustainability professionals. Only one expert focused on hermeneutics or how concepts like ‘impact’ are interpreted.

The results show that some themes are common in the DMA process. For example, those of ‘Focus on effectiveness’, ‘Focus on the strategy of the organization’, ‘Focus on anticipation’, and ‘Focus on compliance’. Attachments 1 and 2 include the first-order concepts identified throughout the data, listed by the interviewee, and classified into the second-order themes mentioned above.

3.2 Challenges when conducting a DMA

The themes related to the challenges associated with the DMA are shown below in Table 2. The results show that the limitation of time and human resources are primary challenges when conducting a DMA.

Table 2. DMA challenges – Themes and total frequency of concepts.

| Themes | Experts | Sustainability professionals |

|---|---|---|

| Consultant-dependent process | 0 | 1 |

| Deficits in reporting quality | 2 | 0 |

| Expertise | 5 | 1 |

| Gap identification & processing | 0 | 2 |

| Lost impact | 2 | 0 |

| Lost material topics | 1 | 0 |

| New sub-process | 0 | 2 |

| Partner selection | 0 | 2 |

| Resource-intensive process | 5 | 6 |

| Tricky topic identification | 0 | 1 |

| Unclear/Need for clarification | 1 | 0 |

| Unfitting to organization | 1 | 0 |

The first-order concepts from where the second-order themes listed above originated include recurring concepts mentioned during the interviews, for example, ‘challenges in finding the right expertise’, ‘conducting a new process’, and ‘cooperation between internal/external partners’. The first-order concepts identified and classified into the second-order themes listed above are listed in Attachments 3 and 4. They include notions like ‘Needing the right specialist to get data’, which was classified under the ‘Expertise’ theme, and ‘Process might be perceived as overwhelming’ classified under the ‘Resource-intensive process’ theme.

4 Discussion

The results presented above show that the process of DMA is seen from several dimensions, especially that of ‘effectiveness’ which is linked to matters of time management, preparation, resourcing, tools, processes, expertise, finance (investments), and consulting. The theme of ‘effectiveness’is salient across both participant groups (experts and sustainability professionals). This is followed by ‘anticipation’ and ‘compliance’. The first is linked to an expectation of change as well as preparation and readiness for it. Concepts related are ‘a larger scope, stepping into the unknown, and thinking about building a foundation for the future.’

4.1 Balancing effectiveness and compliance with strategy and performance

Based on these findings it could be argued that the focus on effectiveness agrees with institutional theory because the emphasis is put on rules, structures, and processes (Roszkowska-Menkes, 2022). The findings point to some phenomena that could be recurring and, thus, some of the challenges and opportunities could be applied to other companies. The DMA process is conducted considering factors specific to the organization. First is the strategy, second the ‘ambitions’ (as mentioned by Expert 3) or aims of the reporting, followed by matters of ‘effectiveness’ like utilization of tools, preparation, resourcing, and prioritization of topics.

Compliance refers, for example, to the obligation to report and disclose the DMA process. The focus on compliance suggests that legitimacy theory (Suchman, 1995) is relevant for companies doing sustainability reporting since they want to maintain and secure credibility through their compliance. The results of this study emphasize the significance of similarities and differences between ‘experts’ and ‘sustainability professionals.’ One similarity is that a relevant challenge is the time-consuming aspect of the assessment. Expert 2 suggests this challenge could be momentary ‘It’s really time-consuming currently’, pointing to an aspiration for streamlining or/and automating the process. One difference identified between the groups is that the experts focus more on the strategy, and the sustainability professionals more on the sustainability performance.

4.2 A critical look at numbers and expertise

The findings show that the DMA could be a ‘resource-intensive process’ that requires significant ‘expertise’ to be conducted. The results show that to tackle the challenges some organizations utilize consultants, hire supporting people, find the right expertise within the company, and develop new processes.

Nevertheless, opportunities can arise from challenges, for instance, those related to the supply chain. An interesting result is linked to changes originating from the DMA. Regarding collaboration with partners, Sustainability Professional 1 comments: ‘So if they can’t give us specific numbers, then we can’t collaborate with them anymore.’ Strategy and business models have the possibility of being affected by the sustainability report since reporting is not about the annual obligation, they continue: ‘it’s also about that continuous follow-up.’

5 Conclusion

The research questions focused on answering how companies in Finland conduct a DMA, and how they approach challenges identified in the DMA process. A sub-question explores the opportunities encountered while conducting the process or as a result of it. In the previous chapter, the author argued that there are three key findings: the balance between effectiveness and compliance with strategy and performance, the differences between ‘experts’ and ‘sustainability professionals’ regarding focus areas when conducting the DMA, and how the challenges related to the DMA process can influence strategy, operations, and business model development.

CSRD involves a practical dimension that requires intense resources in terms of time and expertise. The research offers a contribution for those exploring the topic in the business or academic world. From a practical perspective, this study can be useful for companies that are familiarizing themselves with the CSRD regulation and contemplating the adoption of a double materiality approach to sustainability reporting. SMEs can also be informed of both the DMA process and the challenges and opportunities associated with it. From the academic perspective, deepening theoretical understanding of the theories underpinning the double materiality approach will provide a solid theoretical ground for future research.

Regarding limitations, further generalization of the results requires a larger sample of companies to be studied. In addition, this paper consisted exclusively of a qualitative approach. Future research related to sustainability reporting could benefit from a double approach (qualitative and quantitative). Regarding methods applied specifically to sustainability, Mio et al. (2024, p. 160) argue that ‘qualitative approaches, such as in-depth interviews or case studies, could complement quantitative analysis to uncover motives and reasons for companies’ reporting.

The qualitative approach in this study provided insights that quantitative data would not have provided, for example, matters related to the resourcing for the elaboration of the sustainability report and the challenges involved in it. Further studies could focus on specific industries and geographical areas.

Attachments

Attachment 1. Concepts and themes – DMA process (Experts)

Attachment 2. Concepts and themes – DMA process (Sustainability professionals)

Attachment 3. Concepts and themes – DMA challenges (Experts)

Attachment 4. Concepts and themes – DMA challenges (Sustainability professionals)

Abstract

A voluntary practice in the 20th century, sustainability reporting became standardized and mandatory in the 21st century. Nevertheless, mandatory reporting does not guarantee corporate responsibility. Deficient sustainability reporting can mislead stakeholders and result in inaccurate performance assessments (Herremans, 2020). Research conducted on the Corporate Sustainability Reporting Directive introduced recently by the European Union shows a lack of transparency in sustainability reports (Correa-Mejía et al., 2024). Research shows deficiencies in the disclosure of the Double Materiality Assessment process, key to the new directive (Mio et al., 2024). The purpose of this article is to explore challenges and opportunities encountered when conducting a Double Materiality Assessment. The paper explores this process with data gathered by interviewing a total of six individuals working in fields directly related to sustainability. Three experts and three sustainability professionals were contacted and interviewed from February to November 2024. Findings reveal that understanding of the Double Materiality Assessment process varies, highlighting both the ambiguity of the process and its adaptability to different contexts. Challenges of the DMA process include resource limitations, data structuring, and recognizing impacts occurring in the value chain. The article is part of the author’s article thesis for the MBA in Management in Sustainable Business at Häme University of Applied Sciences (HAMK).

Author

Mily Vázquez Harkivi, graduate of the MBA in Sustainable Business Management at HAMK.

References

Bell, E., Bryman, A., & Harley, B. (2022). Business research methods (6th ed.). Oxford University Press.

Correa-Mejía, D. A., Correa-García, J. A., & García-Benau, M. A. (2024). Analysis of double materiality in early adopters. Are companies walking the talk? Sustainability Accounting, Management and Policy Journal, 15(2), 299–329. https://doi.org/10.1108/SAMPJ-07-2023-0469

De Villiers, C. (2022). New Directions in the European Union’s Regulatory Framework for Corporate Reporting, Due Diligence and Accountability: The Challenge of Complexity. European Journal of Risk Regulation, 13(4), 548–566. https://doi.org/10.1017/err.2022.25

Dinh, T., Husmann, A., & Melloni, G. (2022). Corporate Sustainability Reporting in Europe: A Scoping Review. Accounting in Europe, 20(1), 1–29. https://doi.org/10.1080/17449480.2022.2149345

Eskerod, P. (2020, June 30). A Stakeholder Perspective: Origins and Core Concepts. Oxford Research Encyclopedia of Business and Management. Retrieved 21 Feb. 2025, from https://doi.org/10.1093/acrefore/9780190224851.013.3

European Commission. (2021). Questions and Answers: Corporate Sustainability Reporting Directive proposal. Retrieved 18 Nov. 2024 from

https://ec.europa.eu/commission/presscorner/api/files/document/print/en/qanda_21_1806/QANDA_21_1806_EN.pdf

European Parliament. (2021). Briefing – Non-financial Reporting Directive. European Parliamentary Research Service. EPRS (European Parliamentary Research Service). Retrieved 18 Nov. 2024 from https://www.europarl.europa.eu/RegData/etudes/BRIE/2021/654213/EPRS_BRI(2021)654213_EN.pdf

Fiandrino, S., Tonelli, A., & Devalle, A. (2022). Sustainability materiality research: a systematic literature review of methods, theories and academic themes. Qualitative Research in Accounting & Management, 19(5), 665–695. https://doi.org/10.1108/QRAM-07-2021-0141

Freeman, R. E. (2010). Strategic Management: A Stakeholder Approach. Cambridge University Press.

Friske, W., Hoelscher, S. A., & Nikolov, A. N. (2022). The impact of voluntary sustainability reporting on firm value: Insights from signalling theory. Journal of the Academy of Marketing Science, 51(3), 372–392. https://doi.org/10.1007/s11747-022-00879-2

Fälth, L., & Lindberg, R. (2024). Integrating Double Materiality: As Simple as Ticking a Box [Master’s thesis, Uppsala University]. DiVA. https://www.diva-portal.org/smash/get/diva2:1875695/FULLTEXT01.pdf

Herremans, I. (2020). Sustainability performance and reporting. Business Expert Press.

Jørgensen, S., Mjøs, A. and Pedersen, L.J.T. (2022). Sustainability reporting and approaches to materiality: tensions and potential resolutions. Sustainability Accounting, Management and Policy Journal, 13(2), 341–361. https://doi.org/10.1108/SAMPJ-01-2021-0009

Lee, N., & Lings, I. (2008). Doing business research: A guide to theory and practice. Sage Publishers.

Mio, C., Agostini, M., & Scarpa, F. (2024). Sustainability reporting: Conception, international approaches and double materiality in action. Springer Nature.

Puroila, J., & Mäkelä, H. (2019). Matter of opinion: Exploring the socio-political nature of materiality disclosures in sustainability reporting. Accounting, Auditing & Accountability Journal, 32(4), 1043–1072. https://doi.org/10.1108/AAAJ-11-2016-2788

Roszkowska-Menkes, M. (2022). Institutional theory. In S. Idowu, R. Schmidpeter, N. Capaldi, L. Zu, M. Del Baldo, & R. Abreu (Eds.), Encyclopedia of Sustainable Management. Springer, Cham. https://doi.org/10.1007/978-3-030-02006-4_389-1

Schoenmaker, D., & Schramade, W. (2018). Principles of sustainable finance. Oxford University Press.

Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of management review, 20(3), 571–610. https://doi.org/10.2307/258788

Uwah I. (2024). A critical appraisal of the EU Corporate Sustainability Reporting Directive: Unpacking the double materiality principle. [Master’s thesis, The Arctic University of Norway]. UiT (Universitetet i Tromsø) Munin Open Research Archive. https://munin.uit.no/bitstream/handle/10037/34401/thesis.pdf